| Monday | 10:30 AM – 6:30 PM |

| Tuesday | 10:30 AM – 6:30 PM |

| Wednesday | 10:30 AM – 6:30 PM |

| Thursday | 10:30 AM – 6:30 PM |

| Friday | 10:30 AM – 6:00 PM |

| Saturday | 10:00 AM – 5:30 PM |

| Sunday | 10:00 AM – 5:30 PM |

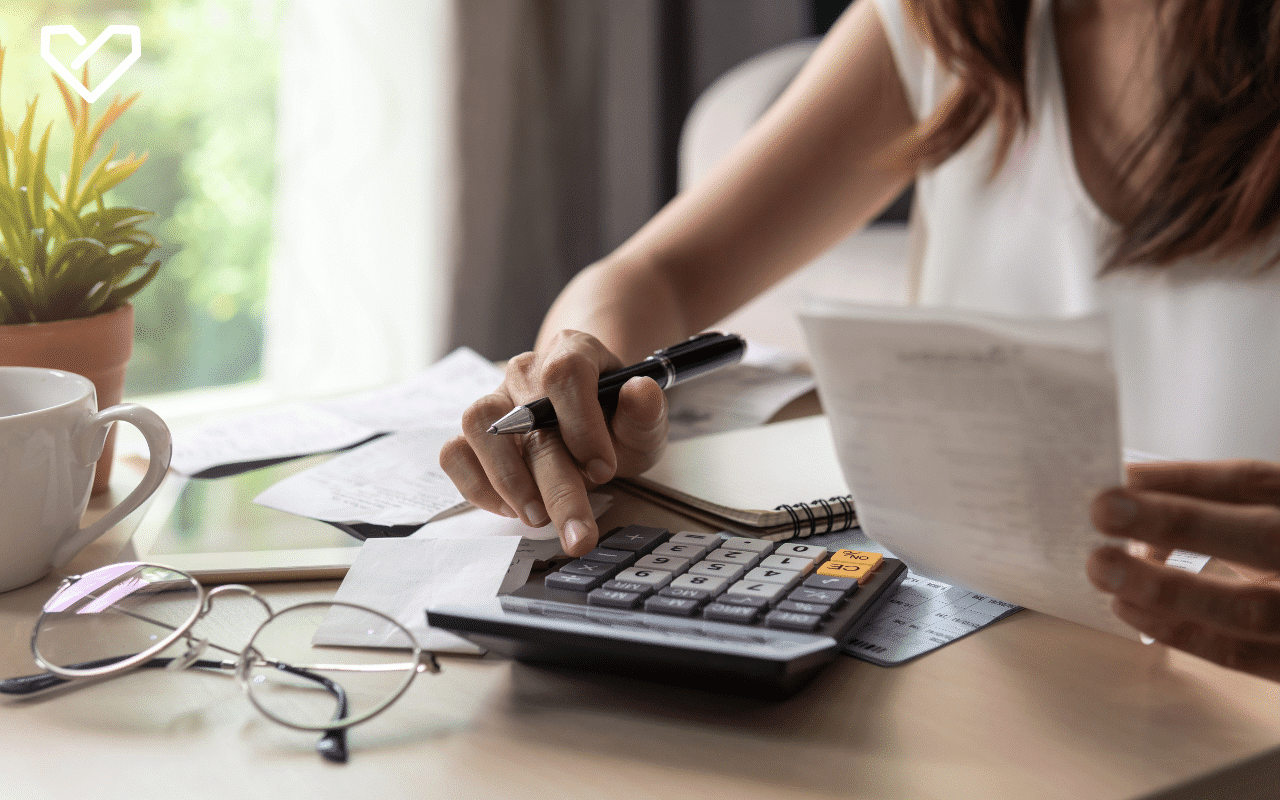

This guide will explain the benefits and drawbacks of making extra mortgage payments. We will examine how it affects your mortgage balance, the amount of interest you pay, and your financial freedom over time.

When you pay more on your mortgage, your mortgage balance lowers quicker, meaning you will pay less interest in the long run.

You can make extra payments by either increasing your regular monthly payments or using a lump sum.

Most lenders allow you to overpay. This amount is usually up to 10% of your outstanding balance each year, especially for fixed-rate mortgages.

Overpayments can make the length of your mortgage shorter, and they can also help you build equity faster.

Always check your lender’s terms to avoid early repayment charges (ERCs).

A mortgage overpayment happens when you pay more than what you owe each month. This extra money lowers your outstanding mortgage balance. By doing this, you can save on the total amount of interest you will pay. It can also help you finish paying off your mortgage term sooner. Overpayments can be:

Monthly overpayments (for example, putting in £100 every month)

Single lump sums (like making a one-time payment of £5,000 from a work bonus)

Making extra payments can help you lower your loan amount quickly. This will lessen the interest you pay in the future. It is especially helpful if you have a higher interest rate.

In 2025, interest rates for mortgages are still high. If your mortgage has a higher interest rate than the savings rate, it might be a good idea to overpay your mortgage. This can give you returns that are better than many savings accounts. Therefore, using any extra money to pay down your mortgage could be a smart choice.

If you have a fixed-rate mortgage with a 5% interest rate and your savings account earns 3%, paying extra on your mortgage can save you money in the long run.

Before you spend more on your mortgage, look at your complete financial situation. It’s important to pay off debts with high interest, like credit cards and overdrafts. Also, make sure to have an emergency fund. This fund should be enough to cover 3 to 6 months of your living costs.

Next, consider your financial goals for the short and long term. Are you saving for something important? Or are you thinking about equity release later on? If that’s the case, putting your money into your mortgage might make it harder to change those plans in the future.

Finally, review your mortgage agreement, read about the overpayment allowance, and check for any fees for early loan repayment.

Most lenders let you pay up to 10% of your outstanding mortgage balance each year without fees. This limit is called your overpayment allowance. For example, if your mortgage is £200,000, you can pay an extra £20,000 in a year without facing any early repayment charges.

If you go over this limit, you may need to pay ERCs. This can happen if you have a fixed rate or a standard variable rate mortgage. It’s essential to read your mortgage documents. You can also talk to your lender to get a better understanding of the terms.

When you pay off your mortgage balance sooner, you can reduce the amount of interest you pay over time. Here is how it works:

If you make overpayments sooner, they will have a bigger impact. This is because of compounding interest.

| Overpayment Type | New Term | Interest Saved |

|---|---|---|

| £50 extra per month | 23.2 years | £11,534.39 |

| £100 extra per month | 21.6 years | £21,142.17 |

| £5,000 lump sum | 23.11 years | £10,011.66 |

These figures are based on a £200,000 repayment mortgage over 25 years at 4.5% interest. Actual savings will vary depending on your mortgage terms, rate, and lender policies.

You can usually make overpayments via:

You can make a bank transfer using your mortgage account number.

A monthly direct debit can be set up with a larger amount.

You can use a debit card for one-time lump sum payments.

Interest Savings: You will pay less in interest over time.

Shorter Loan Term: A shorter length of your mortgage means you can be debt-free faster.

Lower LTV: A lower loan-to-value ratio can provide you with better remortgage choices.

Financial Peace of Mind: Less mortgage debt gives you more financial security.

Better Use of Spare Cash: Using your spare cash is usually better than keeping it in low-interest accounts.

Expert mortgage advice

Liquidity Loss: After you pay, it is tough to get your money back. You can only do this by remortgaging or using equity release.

Early Repayment Charges: Paying more than your overpayment allowance can lead to hefty fees.

Missed Opportunities: Overpaying is not wise if you have high-interest debts, like credit cards or overdrafts.

Reduced Emergency Funds: Don’t stretch your budget too far. Always set aside some money for emergencies.

Before you pay extra, start an emergency fund. This fund should have enough money to pay for 3 to 6 months’ worth of expenses. With this fund ready, you can deal with surprises like losing your job or needing urgent repairs. You won’t have to depend on credit cards or overdrafts.

Use your extra money smartly. If your mortgage interest rate is higher than your savings rate, paying more towards your mortgage can help. However, if your lender charges high fees for early repayments or if your finances are not stable, it might be best to wait before making any extra payments.

When you look at your mortgage rate, think about how it compares to the returns you expect from your investments. If your investments make more money than your mortgage rate, investing might be a better choice for you. On the other hand, if you pay a higher interest rate, it may help you save money and reduce risk.

Consider if you would like to sell equity in the future. Currently, reducing your mortgage debt can help increase your home equity. This might give you more choices later in life.

Deciding whether to pay off your mortgage or keep a small balance really depends on your money goals. Paying off the mortgage completely can give you peace of mind. It means no more monthly payments. This can help you save money for other investments or costs.

Leaving a small balance on your mortgage can help you get lower interest rates on investments. These investments might bring you higher returns than your mortgage rate.

Some people keep their mortgage to take advantage of tax deductions on the interest they pay. In the end, it’s crucial to balance your financial goals. Think about what makes you feel secure and comfortable!

The 10% rule for mortgage overpayment is a helpful guideline. It allows homeowners to pay more on their mortgage. This extra payment helps reduce the mortgage balance. Typically, you can pay up to 10% of the outstanding balance each year. You won’t face any penalties for making these extra payments.

You can pay more on your loan to reduce the total interest you will pay over time. This choice can help you pay off your mortgage sooner. It’s a smart move for anyone who wants to save money in the long run. Just be sure to read your mortgage agreement first. Some lenders have different rules about overpayments!

Paying a little more each month, such as £50 to £100, can reduce your interest and make your loan term shorter. You can adjust this amount depending on your budget.

The best ways to make an overpayment are to use a bank transfer, a debit card, or to set up a monthly direct debit. Make sure to check that the mortgage account number is correct.

Yes, there are limits on how much you can overpay. Most fixed-rate mortgages let you pay off up to 10% of the outstanding balance each year. Make sure to check with your lender about the overpayment allowance.

Paying more than you need to will not directly lower your interest rate. However, paying extra can reduce your LTV. A lower LTV might make it simpler to get a lower interest rate when you remortgage.

It’s a good idea to pay off high-interest debts before anything else. This means you should focus on paying off credit cards and overdrafts first.

Paying more on your mortgage in 2025 can be a good idea. It is best when your mortgage has a higher interest rate than your savings. You should feel secure in your finances too.

This extra payment helps reduce your mortgage balance and shortens your loan term. It will also lower the total amount of interest you pay over time. Just remember to check your lender’s overpayment allowance. Always keep liquidity and your financial stability as a priority.

Think about your debts right now. Also, look at your savings goals and plans for the future before you make any extra payments. Remember, what works for one homeowner may not work for someone else. If you feel unsure, always get expert mortgage advice.

Expert mortgage advice

At New Homes Mortgage Services LLP, we strive to provide accurate and up-to-date information at the time of publication. However, due to the dynamic nature of the property market, details may change and this content is intended for general informational purposes only. It does not constitute financial or professional advice and should not be relied upon as such.

We cannot accept responsibility for any decisions made based on this information. For advice tailored to your individual circumstances, please consult our qualified mortgage advisors. We recommend that you independently verify any important details before making financial commitments.

Subscribe for more mortgage updates

Do you need expert mortgage advice?