What are the different mortgage types?

Buying a home is one of the biggest financial decisions you will ever make, and choosing the right type of mortgage can make a big difference to your monthly payments, your long-term costs, and your peace of mind.

But with so many types of mortgages available in the UK, including options for long-term mortgages that allow you to fully own your own home, how do you know which one is best for you in the long run?

In this guide, we’ll explain the differences between mortgage types and provide insight into each to help you choose the mortgage that helps you get your dream home!

There are several types of mortgages out there, such as:

- Fixed-rate mortgages

- Variable rate mortgages

- Buy-to-let mortgages

- Discount mortgages

- Tracker Mortgages

There are benefits to each type of mortgage, but we know that typically the biggest question is “How much will my repayments be?”

To get an idea of your estimated monthly payments for different types of mortgages, use our Mortgage Calculator. Note your monthly payments will always differ based on factors such as interest rates and deposits.

In this guide, we’ll also help you understand what factors affect your eligibility and affordability for each type of mortgage, such as your credit score, deposit, and income.

Repayment vs Interest-Only Mortgages

The first thing you need to decide is whether you want a repayment mortgage or an interest-only mortgage. These are the two main ways of paying back your mortgage loan.

Repayment Mortgages

A repayment mortgage is the most common type of mortgage in the UK. With a repayment mortgage, you pay back both the capital (the amount you borrowed) and the interest (the cost of borrowing) every month, until you own the property outright at the end of the mortgage term.

The advantages of a repayment mortgage are:

- You build up equity in your home over time, which means you have more security and flexibility if you want to sell or remortgage in the future.

- You know exactly how much you will pay each month and when you will be debt-free, which makes budgeting easier and reduces the risk of falling into arrears.

- You can benefit from lower interest rates if you have a large deposit or a good credit score, as lenders will see you as a lower-risk borrower.

The disadvantages of a repayment mortgage are:

- Your monthly payments will be higher than an interest-only mortgage, as you are paying off both the capital and the interest.

- You may have less disposable income to spend on other things, such as holidays, hobbies, or savings.

- You may find it harder to get approved for a repayment mortgage if you have a low income, a small deposit, or a poor credit history, as lenders will assess your affordability based on your income and outgoings.

Interest-Only Mortgages

An interest-only mortgage is a type of mortgage where you only pay the interest on the loan every month and not the capital. This means that your monthly payments will be lower than a repayment mortgage, but you will still owe the full amount you borrowed at the end of the mortgage term.

This type of mortgage can be beneficial for those who want to reduce the amount of interest they are charged, but it is important to have a solid plan in place to repay the capital, such as selling the property, using savings, or investing in another asset.

The advantages of an interest-only mortgage are:

- Your monthly payments will be lower than a repayment mortgage, as you are only paying the interest.

- You will have more disposable income to spend on other things, such as holidays, hobbies, or savings.

- You may be able to get approved for an interest-only mortgage if you have a high income, a large deposit, or a good credit score, as lenders will see you as a higher-risk borrower.

The disadvantages of an interest-only mortgage are:

- You will not build up any equity in your home over time, which means you have less security and flexibility if you want to sell or remortgage in the future.

- You will have to repay the full amount you borrowed at the end of the mortgage term, which could be a large sum of money that you may not have saved or invested enough for.

- You will be exposed to the risk of interest rate changes, as your monthly payments will vary depending on the market conditions.

Fixed-Rate vs Variable-Rate Mortgages

The next thing you need to decide is whether you want a fixed-rate mortgage or a variable-rate mortgage. These are the two main ways of determining the interest rate you will pay on your mortgage loan.

Fixed-Rate Mortgages

A fixed-rate mortgage is a type of mortgage where the interest rate is fixed for a set period of time, usually between 2 and 10 years. This means that your monthly payments, also known as monthly repayments, will stay the same for the duration of the fixed-rate period, no matter what happens to the market interest rates.

By locking in your mortgage interest rate, you can have stability and predictability in your monthly payments, making it easier to budget and plan for the future. This type of mortgage is especially beneficial for first-time buyers or homeowners looking to secure a good mortgage rate for a set number of years.

The advantages of a fixed-rate mortgage are:

- You have certainty and stability over your monthly payments, which makes budgeting easier and reduces the risk of payment shocks.

- You can benefit from locking in a low interest rate if you expect the market rates to rise in the future, as you will pay less interest over the term of the mortgage.

- You can choose from a range of fixed-rate periods to suit your needs and preferences, such as 2, 3, 5, or 10 years.

The disadvantages of a fixed-rate mortgage are:

- You may pay a higher interest rate than a variable-rate mortgage, as you are paying a premium for the security of a fixed rate.

- You may miss out on lower interest rates if the market rates fall in the future, as you will be stuck with your fixed rate until the end of the fixed-rate period.

- You may have to pay an early repayment charge if you want to switch to a different mortgage deal before the end of the fixed-rate period, which could be a significant amount of money.

Variable-Rate Mortgages

A variable-rate mortgage is a type of mortgage where the interest rate can change at any time, depending on the market conditions and the lender’s discretion. This means that your monthly payments can go up or down, depending on the direction of interest rate changes.

The advantages of a variable-rate mortgage are:

- You may pay a lower interest rate than a fixed-rate mortgage, as you are not paying a premium for the security of a fixed rate.

- You may benefit from lower interest rates if the market rates fall in the future, as you will pay less interest over the term of the mortgage.

- You may have more flexibility to switch to a different mortgage deal at any time, without paying an early repayment charge.

The disadvantages of a variable-rate mortgage are:

- You have uncertainty over your monthly payments, which makes budgeting harder and increases the risk of payment shocks.

- You may pay more interest if the market rates rise in the future, as you will pay more interest over the term of the mortgage.

- You may have less choice of variable-rate mortgages, as some lenders may only offer fixed-rate mortgages or specific types of variable-rate mortgages.

Other Types of Mortgages

Besides the main types of mortgages we have discussed above, some other types of mortgages may suit your specific needs and circumstances. Here are some of the most common ones:

Buy-to-let mortgages

These are mortgages for people who want to buy a property and rent it out to tenants. They usually have higher interest rates and fees than residential mortgages and require a larger deposit and a higher income.

They also have different tax implications and regulations that you need to be aware of.

Discount mortgages

These are mortgages where the interest rate is discounted from the lender’s standard variable rate (SVR) for a certain period, usually between 2 and 5 years.

This means that you can benefit from lower interest rates than the SVR, but you also have to follow the changes in the SVR, which can go up or down at any time.

They may also have higher fees than other mortgages, and the discount may not be very large.

Flexible mortgages

These are mortgages that allow you to make overpayments, underpayments, or payment holidays, without incurring any penalties or charges.

This means that you can adjust your monthly payments to suit your cash flow and financial situation, and potentially pay off your mortgage faster or save on interest.

However, they may have higher interest rates than other mortgages, and you need to be disciplined and responsible with your repayments.

Guarantor mortgages

These are mortgages where a third party, usually a family member or a friend, agrees to guarantee your mortgage repayments in case you default.

This means that you can get approved for a mortgage even if you have a low income, a small deposit, or a poor credit history, as the lender will rely on the guarantor’s financial standing.

However, this also means that the guarantor will be liable for your debt if you fail to pay, which could put their finances and property at risk.

Joint mortgages

These are mortgages where two or more people share the ownership and responsibility of the property and the mortgage. This means that you can combine your income and deposits to get a larger mortgage and a better deal.

However, this also means that you are jointly and severally liable for the mortgage repayments, which means that if one of you stops paying, the others will have to cover the shortfall.

You also need to agree on how to split the equity and the payments, and what to do if one of you wants to sell or move out.

Offset mortgages

These are mortgages where you link your savings account to your mortgage account, and the interest you earn on your savings is used to reduce the interest you pay on your mortgage.

This means that you can save money on interest and pay off your mortgage faster, without losing access to your savings.

However, they may have higher interest rates and fees than other mortgages, and you may miss out on better returns on your savings elsewhere.

Tracker mortgages

These are mortgages where the interest rate tracks a certain benchmark, usually the Bank of England base rate, plus a certain margin. This means that your interest rate will change in line with the base rate, which can be good or bad depending on whether the base rate goes up or down.

They may have lower fees than other mortgages, and they may offer more transparency and fairness than the lender’s SVR. However, they may also have a collar or a floor, which means that the interest rate cannot go below or above a certain level, which could limit your savings or increase your costs.

How to choose the right mortgage for you

As you can see, there are many types of mortgages to choose from, and each one has its advantages and disadvantages. The best type of mortgage for you will depend on your personal and financial circumstances, your preferences and goals, and your expectations and predictions of the future.

Here are some of the factors that you should consider when choosing a mortgage:

Your deposit

The amount of money you have saved up to put towards the purchase of the property. The larger your deposit, the lower your loan-to-value (LTV) ratio, which is the percentage of the property value that you borrow. A lower LTV ratio means that you can access more mortgage deals, lower interest rates, and lower fees, as you pose less risk to the lender.

The minimum deposit required for most mortgages is 5%, but some lenders may ask for more, especially for interest-only or buy-to-let mortgages. You may also be able to get a 100% mortgage if you have a guarantor or use a scheme but these options come with their risks and costs.

Your income

The amount of money you earn from your employment, self-employment, or other sources, such as pensions, benefits, or investments. Your income determines your affordability, which is the amount of money you can comfortably spend on your mortgage repayments every month, without compromising your other essential and non-essential expenses.

Lenders will assess your affordability based on your income and outgoings, and they will usually lend you up to 4.5 times your annual income, or more if you have a high income. However, you should also consider your budget and lifestyle, and not borrow more than you can afford to repay.

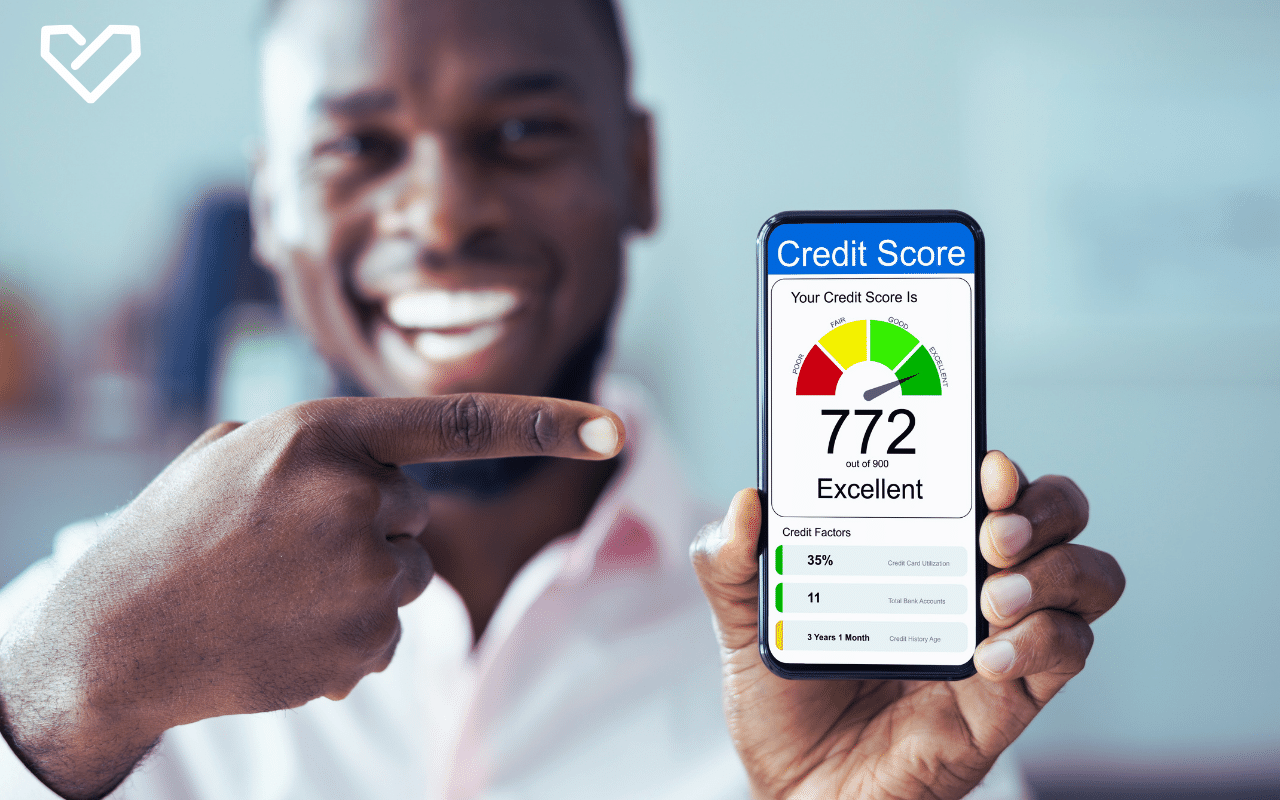

Your credit score

Your credit history shows how well you have managed your past and current debts, such as loans, credit cards, or bills. Your credit score affects your eligibility, which is the likelihood of getting approved for a mortgage by the lender.

Lenders will check your credit score and credit report to see how reliable and trustworthy you are as a borrower, and they will use this information to decide whether to lend you money, how much to lend you, and what interest rate to charge you.

A higher credit score means that you have a good credit history, and you can access more mortgage deals, lower interest rates, and lower fees, as you pose less risk to the lender

A lower credit score means that you have a poor credit history, and you may have fewer mortgage options, higher interest rates, and higher fees, as you pose more risk to the lender. You can improve your credit score by paying your debts on time, keeping your credit utilisation low, and avoiding multiple credit applications in a short period.

Your preferences

The personal choices and opinions that you have about your mortgage, such as how long you want to stay in the property, how much risk you are willing to take, and how much flexibility you want.

Your preferences will influence the type of mortgage that suits your needs and goals, such as whether you want a repayment or an interest-only mortgage, a fixed-rate or a variable-rate mortgage, or a short-term or long-term mortgage.

You should weigh the pros and cons of each type of mortgage, and consider the trade-offs between security and savings, stability and flexibility, and certainty and opportunity.

You should also think about the future, how your circumstances and the market conditions may change over time, and how that may affect your mortgage.

It’s always best to talk to one of our expert mortgage advisors – contact us here